Commercial real-estate is in dire straights.

At the start of the week, a lawyer specializing in advisory services for lenders and servicers of commercial mortgage-backed securities (CMBS) in the United States told us that the office segment of the commercial real estate market has been surprisingly quiet in the first quarter, despite the countless news headlines about towers being dumped on the market for hefty discounts.

The reason for this recent calm in the CRE space might be explained in a note by Vinay Viswanathan of Goldman Sachs on Tuesday.

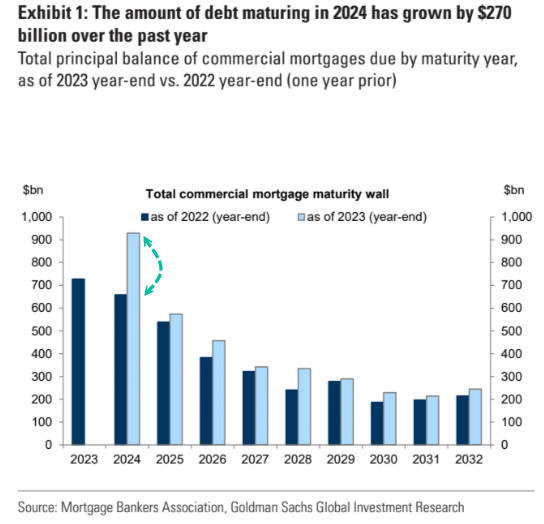

Viswanathan explained that the total amount of outstanding commercial mortgages set to mature by year-end has exploded from $658 billion at the start of last year to $929 billion in mid-March.

He said this high amount of debt that has been extended and modified rather than refinanced “helped mitigate a default wave and a sharp pick-up in losses on CRE loan portfolios.” He noted the main driver of this has been the “willingness of lenders and borrowers to modify and extend maturing loans rather than refinancing or forcing a foreclosure.” In other words, the can was simply kicked down the road until after the presidential elections.

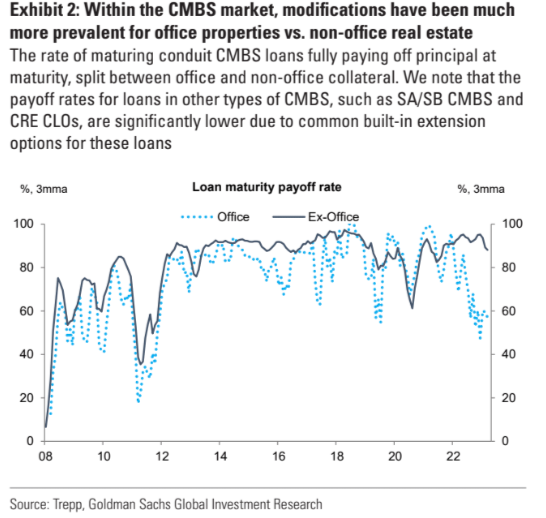

Meanwhile, the stresses are building for the office segment as tower loans that have fully paid off at maturity sink below 60%. However, the maturity payoff rate for loans backed by other property types has been near a decade high.

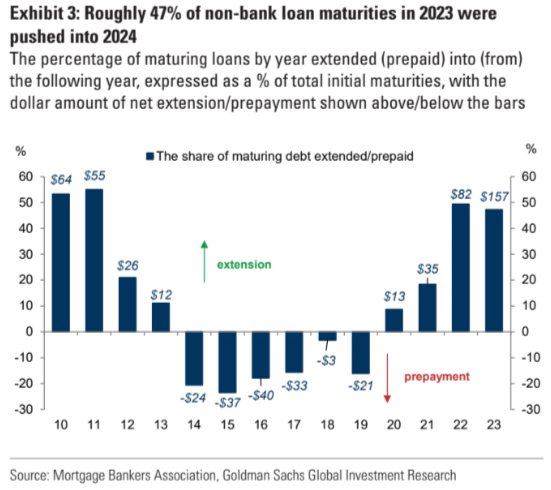

Extend and pretend: About 47% of the non-bank CMBS loan maturities in 2023 were pushed into 2024

The analyst asked how long will the game of musical chairs last:

“While extensions and modifications are not unusual phenomena in the CRE market, particularly during times of rising financial distress and tight lending conditions, the low likelihood that funding costs revert to pre-COVID levels begs the question: how long can this trend continue?”

Viswanathan expects “the wave of modifications to persist in the near term as refinancing stays uneconomical for most commercial real estate borrowers, while foreclosures remain an unappealing proposition for lenders in an illiquid property market.”

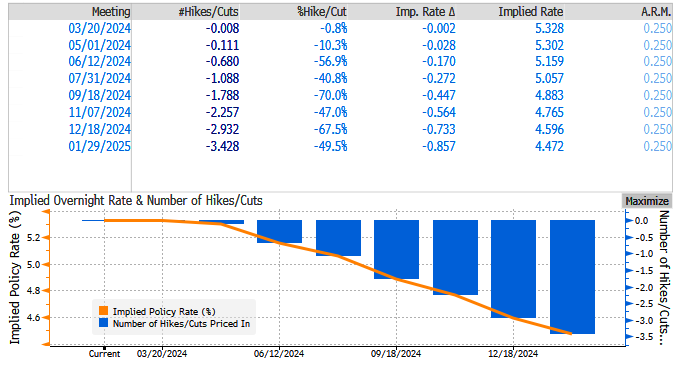

Given that swaps traders and economists at Goldman forecast fewer Federal Reserve interest-rate cuts for the full year and put the odds of a June rate cut around 50%, the higher-for-longer theme suggests risks are undoubtedly surging across the CRE space for 2025.

Viswanathan believes “the risk of a negative feedback loop of distressed sales and lower property prices is largely contained to the office sector.”

EXCLUSIVE: Reporters Expose Nationwide Illegal Immigrant Child Trafficking Operation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}