As the conflict continues to accelerate in Gaza and beyond, 2024 is set for a somewhat terrifying boom in global uncertainty — and will take gold prices with it.

The conflict has escalated to involve neighboring regions, with the potential for further regional destabilization. Israel’s military operations are now focusing on Hamas’ southern and central strongholds, while regional tensions are heightened by the involvement of non-state actors such as Hezbollah, Hamas, and the Iran-aligned Houthis. This threatens regional stability and could also put further pressure on global supply chains if it interferes with Red Sea shipping routes. In response, gold is holding strong after rocketing upward from its October 2023 lows when fighting broke out:

The Biden Administration has vowed to strike back against the Houthis, promising a “sustained campaign” in Yemen that definitively ups the ante on US involvement in the conflict from a proxy war to a direct one. Having barely just finished handing billions to Ukraine in an already-widening fiscal deficit, the escalations in the Middle East carry all the signs of a protracted conflict. Without lenders to finance US involvement, more war that the US can’t afford means more money printing to fund it. As Peter Schiff said late last year:

“Anything that happens over there with Israel, we’re going to get dragged into it. We’re going to be funding it. It’s going to be increasing our deficits, more fiscal stimulus which is inflationary, and that it is going to result in bigger deficits and more money printing — all of this just accelerates the problem now.”

He predicted as much at the start of the Ukraine war and in the Middle East, it’s looking like more of the same. With parallels to 9/11, the October attacks in Israel that launched the conflict could prove to be a 9/11-type “no going back” moment for the region, leading to potentially years of fighting and reshuffling the global chessboard. As Peter Schiff said last October on his podcast, soon after war broke out and gold resumed an upward trajectory:

“The stakes are high, and the implications are serious. Iran’s motives in the background, seeking to disrupt the Israel-Saudi deal. The peace treaty now hangs in the balance, a significant development in an already tense region.”

The election year factor adds another wrench, with an incumbent administration set to embrace war with the hopes of artificially juicing GDP with rising defense stocks. Though disastrous for the people in these countries and terrible for the dollar, all of this meddling points to record highs for gold in 2024 as the world dumps dollars and exposure to US debt and flees to monetary safety.

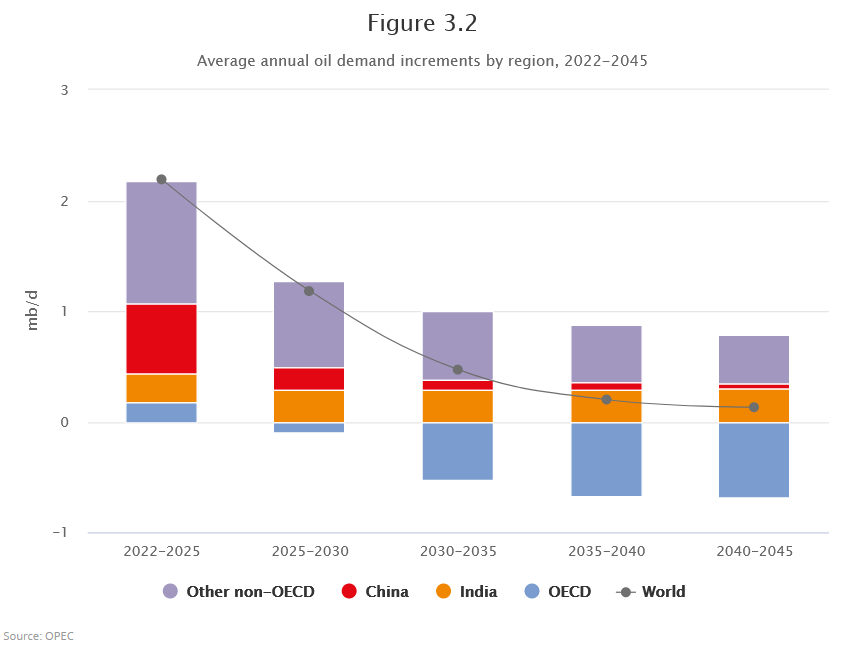

Record domestic oil production in 2024 might be helping provide a small temporary buffer between Americans and higher gas prices as a result of the war and OPEC’s supply cuts last year. Combined with other non-OPEC countries like Brazil and Guyana pumping record amounts, the pressure is on OPEC to get some of that market share back, which could drive oil prices lower still in the near term. However, OPEC still expects demand to skyrocket as it contemplates further cuts due to economic development in China, and pushback on quixotic “net zero” policies driving up the need for fuel between now and 2025.

But current highs in domestic oil production won’t solve the growing US debt bubble and isn’t enough on its own to keep gold prices down. That was true before the fighting started, and it’s even truer as the conflict appears solidly on track to escalate and rip through an already unstable region. Any relief in the price of oil is likely to be temporary, especially as demand increases and money printing to fund the war puts further stress on the dollar.

While the USD is still the “best of the worst” compared to alternatives like the euro, before the war, foreign countries like China were already offloading US Treasuries, and trillions more will soon need to be refinanced. That’s just one wad of gunpowder in the global debt keg that was already looming before the outbreak of war made a bad situation worse:

“In short, the US Treasury is ensnared in a debt trap which can only result in foreigners spurning US Treasuries and the dollar itself.”

In fact, China’s Treasury holdings dropped a whopping 40% last year to prop up the yuan, marking just one factor in the increasing trend of global de-dollarization threatening the USD’s status as the global reserve currency. While some of China’s debt holdings were replaced with mortgage-backed securities, those could encounter trouble as well if the US housing market dumps in the wake of a frothy year for real estate.

The logical outcome of more war, more global uncertainty, a supply crunch for oil, and election year madness? A financial crisis and accompanying global gold rush as dollars get dumped and scores of desperate investors and central banks move to protect their wealth with history’s favorite yellow metal.

Alex Jones: We’ve Moved Beyond The Crossroads, It’s Time To Choose A Side