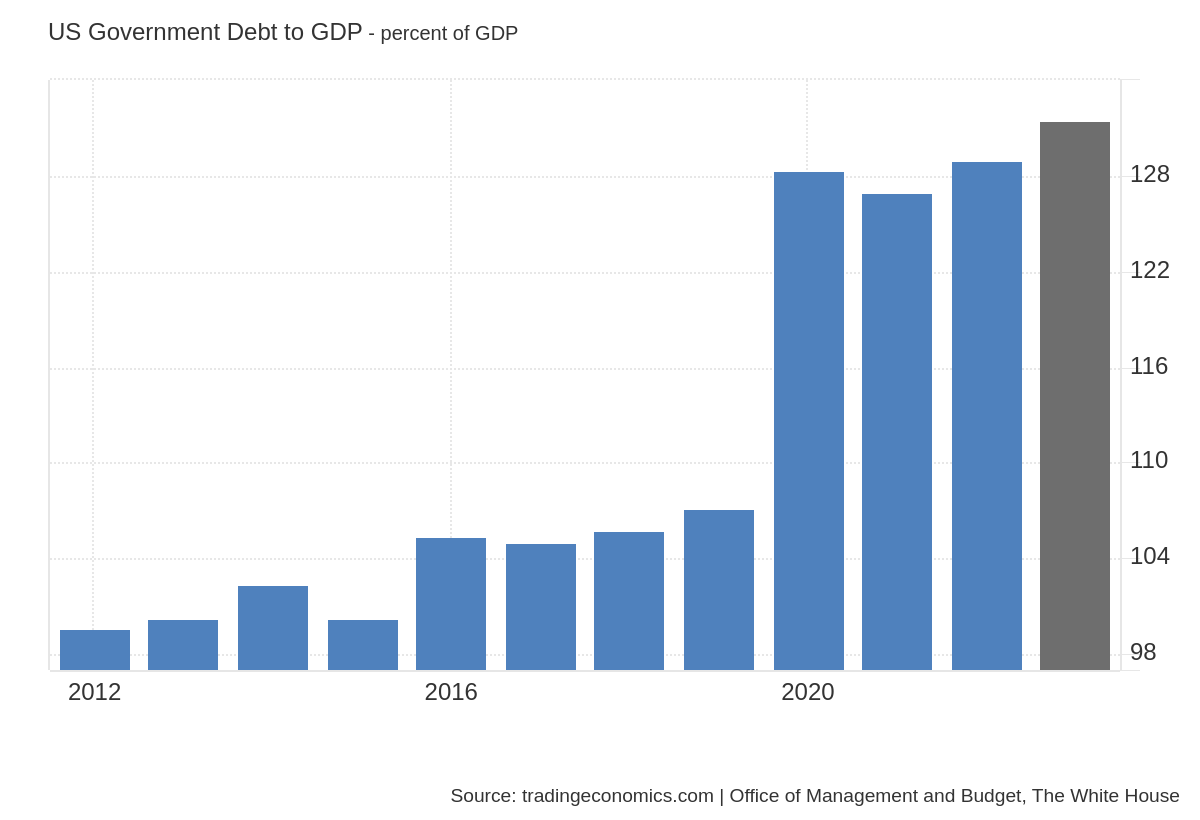

The US national debt is so out of control that, ironically enough, even the Federal Reserve chair has expressed concern about the problem. And while America is among the top contributors, it isn’t just the US that’s spending money it doesn’t have: after briefly declining in 2023, the global debt-to-GDP ratio is again at an all-time high.

Even though interest rates are still extremely low by any free market standard, with even modestly elevated interest rates in the US, payments on servicing the debt skyrocket. This blows up the national debt balloon even bigger. With zero chance of Washington reigning in spending anywhere near enough to keep up, the interest can only be paid with even more borrowing.

The largest quarterly increases were unsurprisingly in the US and Japan, and these are a couple of the most indebted national economies overall. But emerging markets are now along for the ride, with some of the largest debt-to-GDP ratio increases this year coming from the likes of China, India, Brazil, and Mexico. Along with Thailand and Korea, China’s ratio of consumer debt to GDP is still above pre-COVID levels.

In any event, 2023’s debt-to-GPT ratio decline was not due to countries spending more responsibly. It was due to inflation, which can have the effect of boosting nominal GDP, because it increases the total on-paper value of the goods that a country produces, and makes tax revenues appear artificially higher.

But while inflation makes prices go up, it doesn’t increase the real, lasting value of an economy. It also steals purchasing power from savers, which can only be spun as an economic positive in a world like ours, ruled by the Keynesian perversion of fiat central banking. The whipsaw effect of monetary policy never truly addresses the root of any problem it attempts to solve. It requires fallible humans with limited information, limited tools, and endless biases to attempt to micromanage a system of near-infinite complexity.

After post-2008 quantitative easing programs flooded the world with cheap credit, it logically resulted in a flood of investment in poorly-rated governments and companies, encouraging risky borrowing. Justified by the need to “stimulate the economy,” expanding the debt with endless central bank money printing promises to fix a problem that was caused by central banking itself. More recently, COVID money-printing “stimulus” shenanigans even more drastically increased the debt-to-GDP ratio to even more epic levels.

Money printing just happens to also enrich those who happen to be closest to the money printer, and financial firms that can scoop up assets for pennies on the dollar during an engineered bust. Meanwhile, Americans are unable to afford basic goods, racking up massive personal debt in addition to what their government owes.

Struggling consumers are starting to realize en masse that something is very wrong. As Peter Schiff said about the Fed in a recent interview with Don Ma on NTD’s Business Matters:

“If it tries to tries to fight inflation, which is worrying the consumer, it’s got to raise interest rates, but that’s already worrying the consumer…on the other hand, if the Fed…cuts them as planned, inflation’s gonna get a whole lot worse, which means consumer confidence can only go down.”

To make matters worse, the current record level of credit card debt being racked up by struggling Americans doesn’t even count the increasingly popular “pay-as-you-go” programs, which aren’t tracked as part of the overall consumer debt calculation. That’s because they’re individual programs offered by retailers, rather than “official” debt that comes from bank loans.

US credit card debt has reached more than $1.1 trillion, an all-time high.

Year-over-year growth has fallen from nearly 40% to 7.5%. It is still much above the historical average, though.

Meanwhile, interest rate on credit card debt is at record 21.6%

Chart: Liz Ann Sonders pic.twitter.com/0XTYf1KweQ

— Global Markets Investor (@GlobalMktObserv) May 9, 2024

In a few other countries (like Canada and Australia), household debt as a percentage of GDP was even higher in 2022 than in the US — over 100% — with no end in sight. A few Western countries, like Germany and Switzerland, have seen their national debt-to-GDP ratios decrease in 2024, but not nearly enough to offset the overall global increase.

The increasing age of the average global citizen is also exacerbating the global debt powder keg. Labor shortages will increase as populations get older and countries don’t have enough young people to employ and replace elderly folks who are aging out of the workforce. Older citizens also require more social services, but without enough revenue to fund them, the entire balance falls apart. Japan has an especially dire issue with an aging population, but even here in the US, the number of Americans expected to hit 65 and up is slated to increase by 47% by 2050.

The recent CPI report indicates that the Fed could be cutting rates in September, but whether they cut or not, America’s debt will continue to expand unsustainably. And the debt bubble is global — when it pops, it’s going to be spectacular.

Economist Peter Schiff Predicts A Financial Crisis That Will Make The Great Depression Look Tame